User Rating: 2 / 5

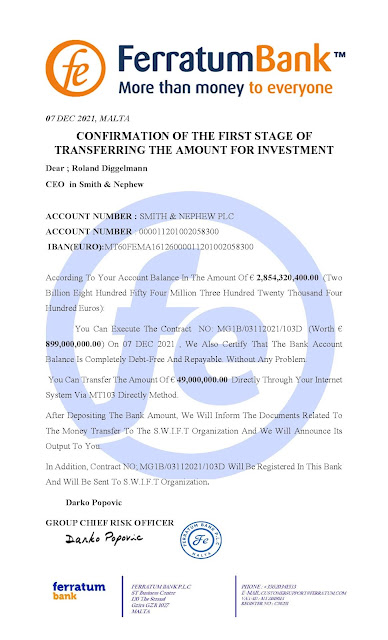

We have been warning the financial industry about the dangers of seeking to obtain a Standby Letter of Credit for decades, but we still see legitimate businessmen paying huge fees to secure one for a major transaction, and always experiencing a loss as the direct result. For the benefit of those who are not familiar with the term, a Standby Letter of Credit is defined as a legal document that guarantees a bank's commitment of payment to a party, in the event that the other party defaults on an agreement. Basically, it is paid when certain conditions have not been fulfilled. An SBLC functions as a guarantee of payment.

It is distinguished from an Irrevocable Letter of Credit, which is a guarantee of payment when certain specified conditions are met, and supporting documents are received by the bank.

Here's the problem; it is literally impossible to fulfill all the terms and conditions of an SBLC within the time frame required in the document. Victims who pay an obscene amount of money to obtain one find, to their dismay, that they cannot sufficiently comply with the complex terms in a timely manner. therefore, the SBLC becomes useless, and the desperately needed funds promised in the SBLC are never paid out by the bank. Many financial crime experts point out that an SBLC is truly a license to steal; it will never be paid to those who purchase them in good faith.

Those who offer SBLCs to the financial community know very well that their clients will never collect the funds offered by the financial instruments they sell. Banks are free to offer SBLCs without fear of regulatory action against them, because so long as the buyer knows what the requirements for payout are, they are legitimate financial products, it's just that you can't collect.

Contributed by Kenneth Rijock - Financial Crime Consultant

Archives of Zen Mahler - Financial Crime Specialist

Chronicles of Monte Friesner - Financial Crime Analyst